In response to Russia’s invasion of Ukraine, a group of democratic nations is imposing economic sanctions against Russia. The punitive measures include a financial sanction in the form of exclusion of some designated Russian banks from the Society for Worldwide Interbank Financial Telecom (SWIFT), which is a Western bloc-led messaging system used for international money transfers.

Of the financial messages exchanged via SWIFT, those related to U.S. dollar-denominated transfers accounted for 42.71% as of April 2023, compared with the shares of 31.74% for euro-denominated transfers, 6.58% for U.K. pound-denominated transfers, 3.51% for yen-denominated transfers, and 2.29% for yuan-denominated transfers. As the designated Russian banks cannot conduct international settlements denominated in the dollar, which has the dominant share, the financial sanction was expected to be effective.

However, some of the Russian international payments excluded from SWIFT were executed directly or diverted to the Cross-Border Interbank Payment System (CIPS) for yuan-denominated settlements, which was introduced by the People’s Bank of China (the Chinese central bank) as a fallback option. As a result, the yuan and the Russian ruble are apparently starting to increase their presence as a currency for international settlements at the expense of the dollar. The effectiveness of the sanctions against Russia appears to be questionable because not only the economic sanctions but also the financial ones are riddled with loopholes.

Furthermore, it has been pointed out that because of the effects of the decrease in the use of the dollar for international financial settlements due to both the exclusion of Russia from the network of dollar-denominated settlements and the increase in the use of the yuan, the dollar key currency system may lose stability.

◆◆◆

The dollar key currency system started under the Bretton Woods regime after the end of World War II. Under this system, a gold-dollar standard was adopted, with the U.S. monetary authority linking the dollar’s value to gold while the monetary authorities of other countries pegged their currencies to the dollar as a way to maintain exchange rate stability. In this way, the dollar became an international currency with the dominant share in currencies held across the world: that is, the key currency.

Because of the Nixon Shock in 1971, the dollar key currency system disappeared as a formal arrangement. However, under the general exchange rate floating system introduced in 1973, the dollar key currency system has in effect continued, with the bulk of international financial settlements conducted in the dollar, a practice which is selected voluntarily by private economic agents.

Why is the dollar the currency of choice for private economic agents despite the loss of its formal status as the key currency? Let’s compare the dollar and other international currencies in terms of the functions that they perform (as a medium of exchange and as a store of value). International currencies are capable of serving as a measure of value (as an invoice currency) as well, but that function will be excluded from discussion here because international currencies selected due to their function as a medium of exchange usually function as a measure of value at the same time.

To examine the dollar’s function as a store of value, let us look back at how its value has changed in terms of the real effective exchange rate as narrowly defined, which is published by the Bank for International Settlements (BIS). By this yardstick, the dollar’s current value is almost the same as the level in 1973, when the general floating system was introduced, so it cannot be said that the dollar has been trending up over time. The dollar has been volatile, sometimes deviating far from the trend line, which means that the dollar is not necessarily superior to other international currencies as a medium to store value from the viewpoint of its stability as a currency.

The dollar is favored as a currency of choice because of its superiority to other currencies as a medium of exchange. For an international currency to function as a medium of exchange, it must have “general acceptability”—that is, the currency must be acceptable by any transaction counterparty at the time of settlement. For an international currency to have general acceptability, the necessary condition is that the currency can be owned and used freely. Foreign exchange control, which imposes restrictions on foreign exchange trading, undermines general acceptability. General acceptability, which is a sufficient condition for a currency to become a key international currency, increases when the foreign exchange market has a certain depth and is highly liquid.

◆◆◆

Here, I will explain the results of an empirical analysis conducted to examine the degree of the dollar’s relative superiority as a medium of exchange. By holding an international currency, private economic agents obtain benefits or utility from the currency’s function of facilitating international financial settlements as a medium of exchange, while they face the risk of incurring cost in the form of depreciation of the real balance of international currency due to inflation.

Based on data concerning the shares of international currencies and the rate of depreciation of the real balance of international currencies, I estimated each international currency’s relative contribution to the utility. The shares of international currencies represent the shares in the balance of debts denominated in domestic and foreign currencies in the Euro currency (offshore) market as compiled by BIS, and the rate of depreciation of the real balance of international currencies is based on an inflation rate projected under a time-series model.

The analytical results showed that the dollar’s contribution to the utility was 54.4% (compared with 27.2% for the euro and 5.6% for the yen) between the first quarter of 1986 and the second quarter of 2016, confirming that the dollar is the dominant international currency.

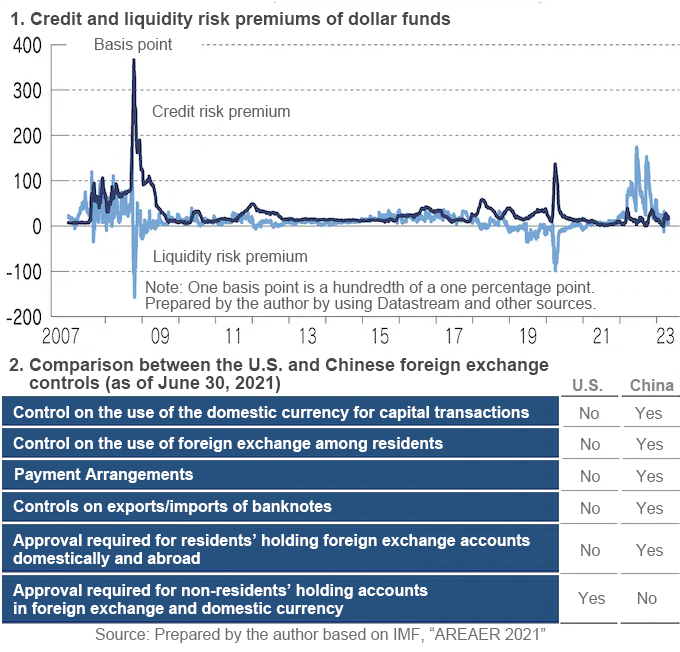

The above figure shows changes in the risk premiums regarding the creditworthiness and liquidity of dollar-denominated interbank funds (with a three-month term). The credit risk premium represents the interest rate differential between the London Interbank Offered Rate (LIBOR), which involves credit risk because of the absence of collateral, and the Overnight Index Swap (OIS), which is relatively risk-free. The liquidity risk premium represents the interest rate differential between the OIS and U.S. Treasuries, which are significantly different from each other in terms of the overall trading scale (which is an indicator of liquidity).

At the time of the global financial crisis in 2007-2008, both the credit risk premium and the liquidity premium rose because of an increase in the counterparty risk (risk of a transaction counterparty failure) involved in interbank transactions. A dollar liquidity crisis occurred, with banks that needed dollar funds facing a lack of counterparty banks willing to supply funds. Around the first half of 2007, when the liquidity crisis broke out, the dollar’s relative contribution to the utility still remained high, at around 50%, despite falling around 5 percentage points, from 54.9% to 49.4%.

Since March 2022, when the U.S. Federal Reserve Board made a policy shift to monetary tightening, the credit risk premium has not risen, but the liquidity risk premium has increased again. That indicates that demand for dollar-denominated funds has remained robust while the supply of dollar-denominated funds has shrunk due to the monetary tightening.

As mentioned earlier, foreign exchange control imposes restrictions on foreign exchange trading, and it therefore undermines the general acceptance of international currencies. The above table shows a comparison of the U.S. and Chinese foreign exchange controls as represented by the status of major foreign exchange transactions based on the Annual Report on Exchange Arrangements and Exchange Restrictions (AREAER), compiled by the International Monetary Fund. In China, most foreign exchange transactions are subject to restrictions. On the other hand, in the United States, foreign exchange transactions are in principle not subject to restrictions except for the cases of account blockade measures imposed against countries subject to the economic sanctions, such as Syria, North Korea, Iran, and Russia, for national security reasons.

So long as China continues to impose restrictions on foreign exchange trading, the yuan does not satisfy the necessary condition for general acceptability and it is therefore far from being a superior international currency as a generally acceptable medium of exchange. If China removes the restrictions on foreign exchange trading in the near future, as the group of democratic nations have already done, it may satisfy the necessary condition for general acceptability, but it must also satisfy a sufficient condition for general acceptability in terms of liquidity.

The arrival of the euro in 1999 caused structural changes to the international currency regime. However, while the euro satisfies the necessary condition for general acceptability, it has not satisfied the liquidity condition for general acceptability as fully as the dollar. The dollar still retains its position as the key international currency. It is safe to assume that the impact of moves to shift away from dollar-denominated international financial settlement as a fallback option will be limited and that the dollar key currency system will remain rock-solid for a while to come.

* Translated by RIETI.

May 22, 2023 Nihon Keizai Shimbun