Economists increasingly stress the importance of investment in intangibles such as human and knowledge capital as a way to stimulate economic growth. This column examines how intangibles contribute to economic growth in Japan and Korea. Though intangible investment has increased in both countries in recent decades, the amount of tangible investment has been greater. This is different from what is observed in western advanced economies, which can be explained by the less developed financial markets in eastern Asia.

Since the Global Crisis of 2008, advanced economies have suffered from low economic growth. Economists and policymakers are increasingly paying attention to the accumulation of intangibles as a new source of economic growth.

The OECD (2013) emphasised that the effects of intangibles on productivity growth are greater than those of tangibles. In Japan, the Shinzo Abe Cabinet is promoting productivity growth in the service industry. The role of intangibles such as human capital and knowledge capital are emphasised in several government reports, such as the White Paper on the Japanese Economy and Fiscal Policy and the White Paper on International Trade and Industry. These reports showed how intangible investment contributed to productivity growth in Japan.

Economists have paid attention to intangibles as key assets that link ICT assets to productivity growth. When Corrado et al. (2009) measured intangible investment at the aggregate level in the US for the first time, the concept of intangibles covered not only R&D but also software, copyrights, brands, firm-specific human capital, and organisational change.

One of the major results of the study was to show the contribution of intangibles (that had been hidden in the contributions of capital assets and total factor productivity) to economic growth, and that the growth in the early 2000s was attributable to the growth in intangible assets.

Intangible investment in Japan and Korea

Following Corrado et al. (2009), we measured intangible investment in Japan and Korea to examine how intangibles contribute to economic growth in East Asian countries. Although the manufacturing sector has led the productivity growth in Japan and Korea, both countries have suffered from low productivity in the service sector. Then, we examined the effects of intangibles on economic growth not only at the aggregate level but also at the sector level in Chun et al. (2015).

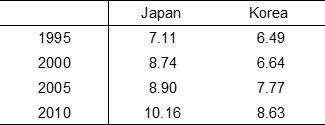

Table 1 shows the ratios of intangible investment to GDP in the market economy for Japan and Korea. Intangible investment increases in both countries and neither ratio is any lower than other western advanced countries. One of the interesting features of intangible investment in both countries is the large share of R&D in intangible investment as a whole, equal to 30% in Japan and 40% in Korea--larger than those in advanced western countries. (Note 1)

- However, in the case of Japan and Korea, the amount of tangible investment is greater than that of intangible investment.

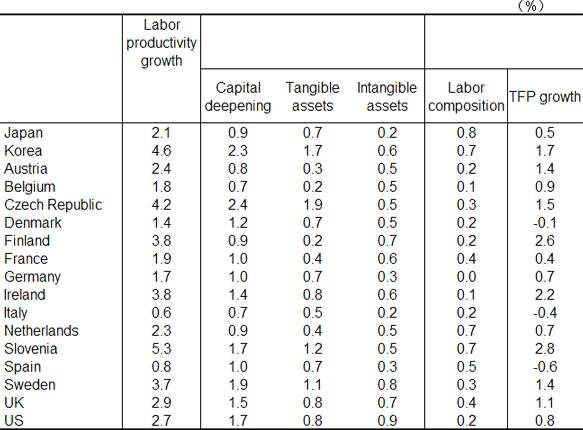

In Table 2, we find that the contribution of tangible assets to productivity growth is greater than that of intangible assets in both countries. While the contribution rates of intangibles are almost the same as those of tangibles in many western countries, the rates of contribution of intangibles are about one third of those in tangibles in Japan and Korea. In particular, the rate of contribution of intangibles in Japan is the lowest among the advanced countries.

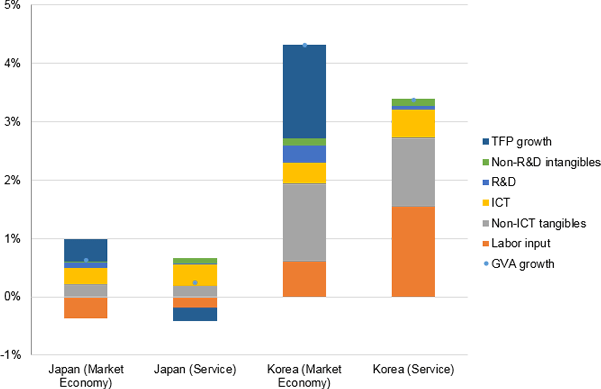

Tables 1 and 2 imply that the contribution of intangible investment to economic growth depends on the composition of intangibles and the industry structure. Figure 1 shows growth accounting in the market economy and service sector in Japan and Korea. In both countries, we find that the GDP growth rate in the service sector is lower than in the market economy, and moreover, the TFP growth in the service sector is much lower than in the market economy. We also find that the accumulation in ICT assets is a main driver of economic growth in the service sector. The problem is that the contribution of R&D and non-ICT intangibles is much smaller than that of ICT assets, in particular, in the service sector. This result implies that intangibles are likely not enough to play a complementary role to ICT capital.

Concluding remarks

Our findings using the analyses in Chun et al. (2015) show that the contributions of intangibles in East Asian countries differ from western advanced countries. The primary reason is that financial markets in both countries are not as developed. As Pyo (2008) pointed out, financial institutions prefer tangible assets to intangible assets because of the former's higher collateral values. If the governments of Japan or Korea wish to promote productivity growth in the service sector through accumulation in intangibles, they have to construct a financial market and accounting system where investors are able to evaluate intangibles explicitly.

This article first appeared on www.VoxEU.org on October 9, 2015. Reproduced with permission.