The war in Ukraine has suddenly increased geopolitical risks. This column argues that firms will respond to the shock by reassessing security-related risks, leading to changes in the structure of supply chains. But given the capital in place, the cost of searching for alternatives, and factors such as wage differentials across countries, this process is likely to be gradual rather than sudden and will affect different sectors and products differently. It will not result in a reversal of globalisation, unless it is supported by pronounced government intervention.

Editors' note: This column is part of the Vox debate on the economic consequences of war.

The war in Ukraine exposes once more the risks associated with the interconnected nature of global trade. The reliance on foreign input producers can lead to the disruption of production when source countries experience a negative shock, such as a war that leads to economic sanctions. Several observers argue that firms will respond to this shock – and the geopolitical tensions it triggered – by reconsidering the balance between efficiency and security, leading to long-term changes in the structure of global value chains (GVCs) in the form of reshoring or nearshoring (e.g. Posen 2022). Similar to the debate on the long-term consequences of Covid-19 (Javorcik 2020, Kilic and Marin 2020, Lund et al. 2020), the recurring question is whether these shocks will lead to the corrosion or even the end of globalisation.

In recent work (Ruta 2022), I use a simple framework to gain some insights on the long-term effects of the war in Ukraine on global value chains. The upshot is twofold. As geopolitical risks have increased in several countries, firms may respond to the shock by revising the structure of their supply chains. This reorganisation away from countries perceived as riskier will affect different sectors and products differently. But the same technological and economic factors that have underpinned the international fragmentation of production in recent decades make a reversal of global value chains unlikely, unless policies radically change.

Changing geopolitical risks

The war has direct effects on the firms operating in Russia and Ukraine and on firms relying on suppliers from those markets (Winkler et al. 2022). But the shock caused by the war goes well beyond these two countries, as geopolitical risks have increased globally. The global Geopolitical Risk Index (Note 1) (Caldara and Iacoviello 2022) has more than doubled since the beginning of the year, reaching levels not seen since the outset of the war in Iraq in March 2003. The data also show substantial changes in geopolitical risks in several economies that are more integrated than Russia and Ukraine in global value chains, including China, Finland, Sweden, Taiwan, among others, pointing to changing perceptions on the risks of future conflicts and sanctions (Figure 1).

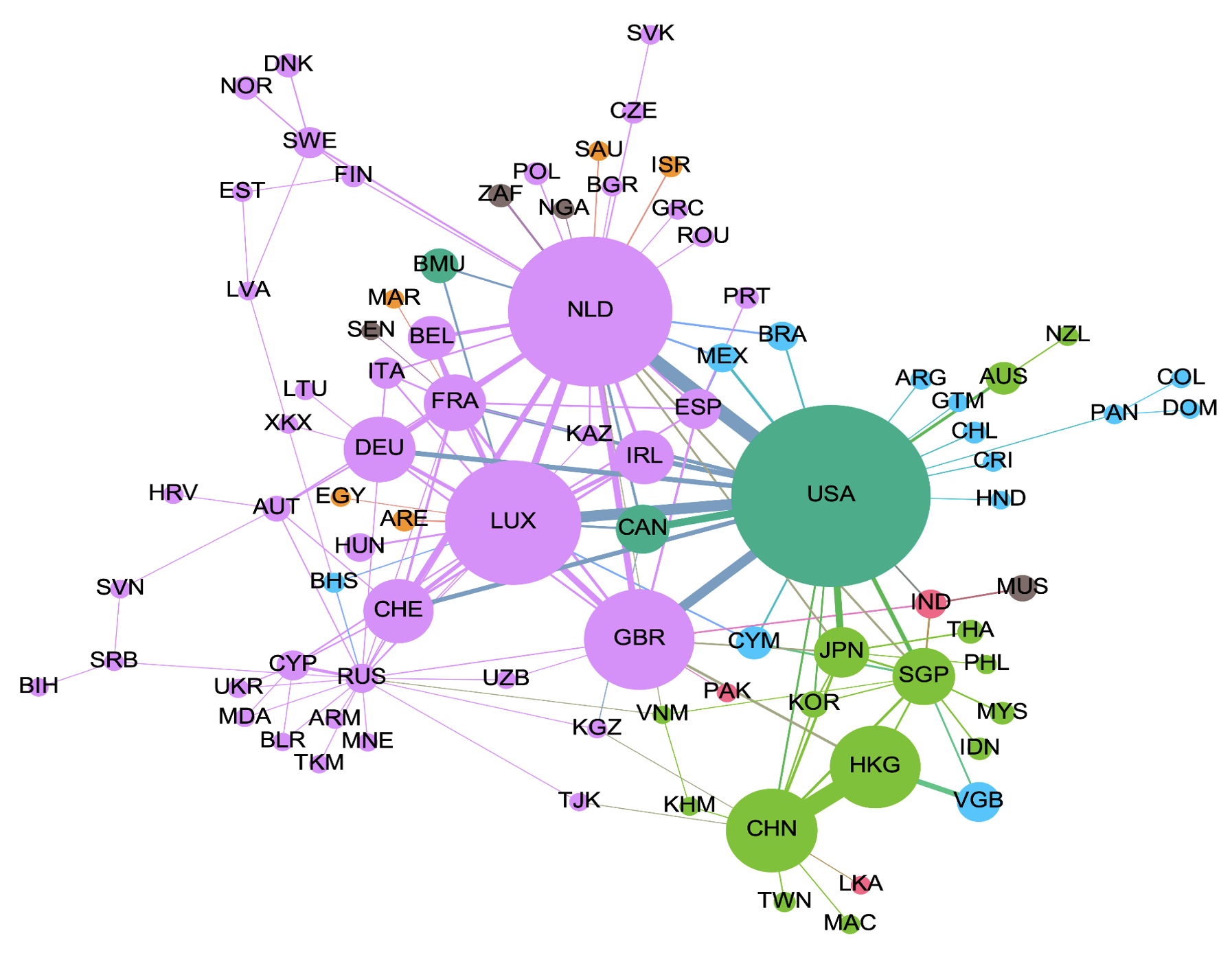

Figure 1 The global network of foreign direct investment

Source: Liu (2022)

How do firms respond to higher geopolitical risks?

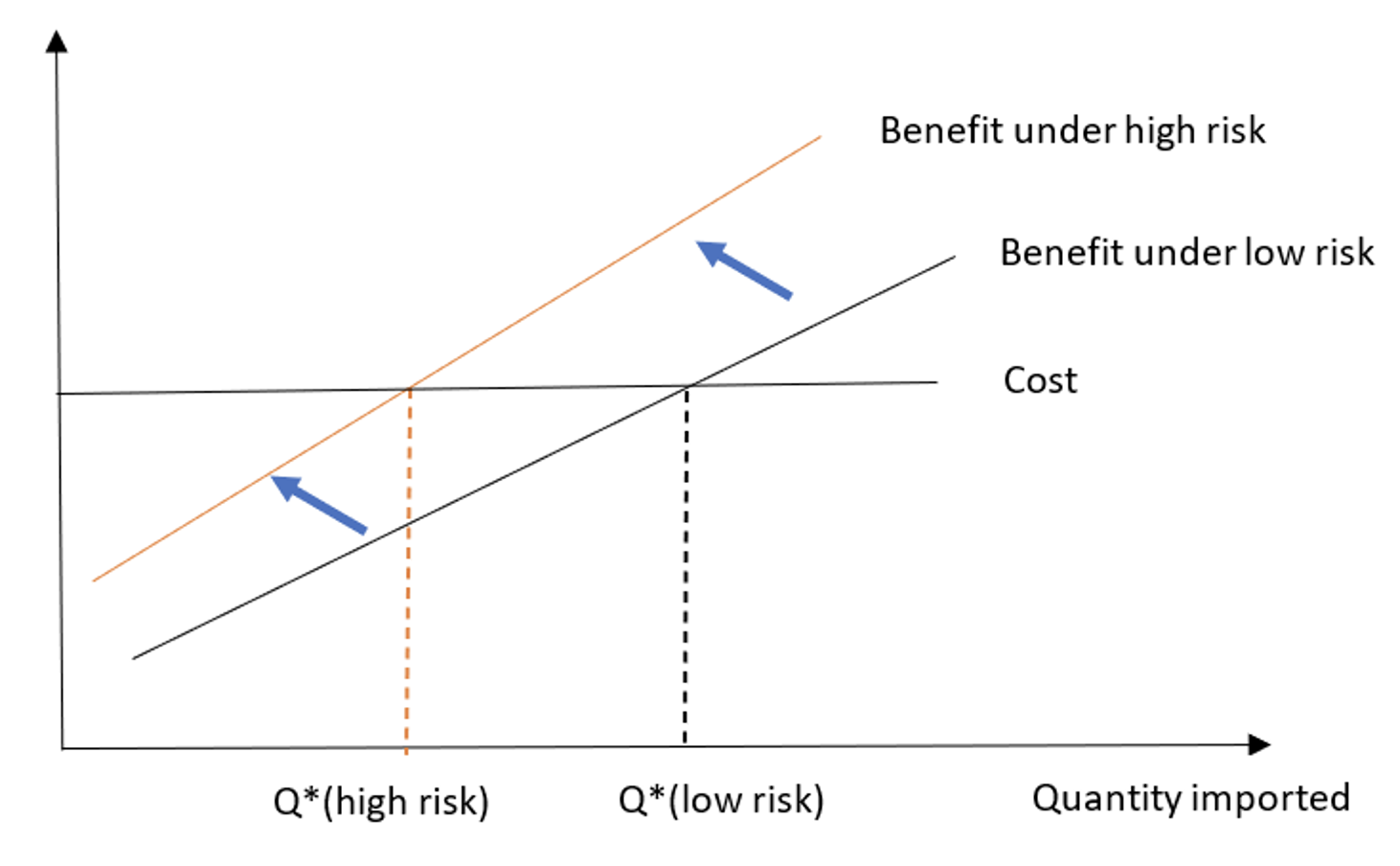

To fix ideas, Figure 2 (based on Freund et al. 2021) focuses on the relocation choice from the perspective of a multinational firm (but a similar logic applies to arm’s length trade). Assume that the firm imports key inputs from a subsidiary in a foreign country and that a geopolitical shock creates security concerns in that country. Under what conditions does the new risk lead the multinational firm to move its subsidiary to a new location?

The firm’s decision to relocate production is determined by a cost-benefit analysis. The benefit of relocation depends on the subsidiary’s scale of production in the foreign country as more exposed firms will be more affected by production disruptions. Its inclination also depends on the per-unit cost difference, which captures factors like the wage differential between the different locations, and the per-unit insurance premium difference, which captures the insurance cost that a firm must pay to cover the risk of production disruptions due to geopolitical or other shocks. The benefit of relocation is compared to the cost, as relocation would entail building a new factory and establishing new relationships in a different location.

A surge in geopolitical risk increases the per-unit insurance premium difference, making the benefit schedule steeper (implying that more exposed firms will have to pay more for insurance). As the old location is suddenly riskier, relocating to a new low-risk location becomes more attractive. The other factors, such as per-unit cost differences between locations and the relocation costs, are not affected by the shock. In the new equilibrium, where the security concern is high, more exposed multinational firms – i.e. those that source from the foreign country more than Q*(high risk) in Figure 2 – relocate their subsidiaries. Those that source less than Q*(high risk) have no incentive to leave even after the geopolitical shock.

Figure 2 Benefits and costs of switching import sources induced by changes in geopolitical risks

How the war may reshape global value chains

This simple framework brings some insights on the current debate on the war and deglobalisation.

First, the war will reshape global value chains, particularly for firms that rely heavily on countries where geopolitical risks have surged, but this does not imply the end of globalisation. Higher geopolitical risk raises the insurance premium that firms need to pay to cover the risk of future production disruptions due to economic sanctions or conflict. For a firm, the risk of disruption rises alongside its reliance on imports from the country at risk, so more exposed firms are more likely to leave. But several factors create inertia, suggesting that a reshaping of some global value chains does not imply sudden deglobalisation. Cost differentials between countries are not affected by geopolitical risk. This makes reshoring to high-cost countries unlikely. Relocating production is also expensive, due to the sunk cost of building new infrastructure and the search cost of establishing new relationships in a different country.

Second, the war-induced reshaping of global value chains will affect different sectors and products differently. Sectors with higher fixed costs and sophisticated intermediate products are less likely to relocate in response to higher geopolitical risks – unless policy intervenes. Firms in an industry like autos, which requires high upfront investment in infrastructure, and firms that rely on sophisticated intermediate products, which rely on relationship-specific investment, face higher costs of relocating production and are thus less likely to leave a country in presence of higher geopolitical risk. Even if the nature of the shock differs, this intuition is confirmed by evidence on the reconfiguration of global value chains in the aftermath of the 2011 Japan earthquake (Freund et al. 2021). Firms in those sectors and products may not reorganise production based only on market incentives, but rather if they expect a change in the policy stance that affects trade costs.

What role for policy?

The world economy will be hurt by the reshaping of global value chains induced by higher geopolitical risks, but some countries will gain and others lose. As firms adjust their production and trade structure to the new environment in the pursuit of economic efficiency, they may seek new suppliers in developing countries that have a latent comparative advantage and lower geopolitical risks. While the high-risk economies, and the global economy as a whole, are worse off in a more uncertain world, the new suppliers would benefit from the increased investment and trade opportunities. In this context, the true risk comes from measures that aim at reshoring, nearshoring, or fragmenting the trade system. Rather, government policies should focus on defusing tensions and strengthening global value chains against future disruptions.

Authors’ note: The views expressed in this column are those of the author and they do not necessarily represent the views of the World Bank Group.

This article first appeared on www.VoxEU.org![]() on May 05, 2022. Reproduced with permission.

on May 05, 2022. Reproduced with permission.