Corporate Japan is known for avoiding uncertainty. This is one of the reasons why changes of any kind are difficult--but not impossible--to realise. This column employs firm data to show that foreign direct investment has been changing corporate Japan by pursuing risk taking in private Japanese firms. This risk taking is positively related to firms' sales growth and corporate earnings.

"In corporate Japan, a lot of time and effort is put into feasibility studies and all the risk factors must be worked out before any project can start. Managers ask for all the detailed facts and figures before taking any decision" (Hofstede 2001).

According to Hofstede's analysis, Japan is one of the most uncertainty-avoiding countries. Indeed, Japanese firms exhibit the lowest level of risk taking in the cross-country analysis of John et al. (2008).

Increasing globalisation recently has been changing corporate Japan. For example, there are hundreds of foreign-owned corporations located in Japan. Foreign investors (companies) bring different technologies and management skills into the foreign-owned firms (Kimura and Kyota 2007, Fukao et al. 2006).

Also, studies on the roles of international institutional investment show that foreign institutional investors export good corporate governance practices around the world and that monitoring and activism by foreign institutions lead to better firm performance (Aggarwal et al. 2011). Thus, financial globalisation and liberalisation strengthen market forces to promote good corporate governance practices and change corporate cultures regarding risk taking.

Risk taking in private firms

Entrepreneurs are thought to be capable of innovation and risk taking. Innovation and risk taking are widely viewed as critical components to the success of any economy. Also, most private companies are run by entrepreneurs, but few studies focus on risk taking in private firms.

Unlike publicly traded firms with dispersed ownership, entrepreneurs are less likely to avoid value-enhancing risky projects in the context of preserving private benefits, as addressed in the seminal work of John et al. (2008). On the other hand, entrepreneurs are likely to invest more conservatively unless they hold a diversified portfolio of firms. Also, bankruptcy laws protect the assets of debtors from creditors, thus risk taking in private entrepreneurial firms strongly depends on the harshness of the consequences of personal bankruptcy laws. In Japan, entrepreneurs usually pledge their residential properties as collateral, and their spouse and relatives provide unlimited liability guarantees as co-signers for entrepreneurial small businesses (Ono and Uesugi 2009).

If a private enterprise is affiliated with its parent company, the intensive monitoring of the parent company dampens the magnitude and the importance of private benefits to the manager. Also, earnings are siphoned out and losses are absorbed by the parent company. The argument of divergence of control and cash flow rights in publicly traded firms with a pyramid ownership structure is not applicable to private affiliated firms. Furthermore, it is possible for the parent to delegate authority and accountability to affiliated firms (e.g. Ito et al. 2008), and this might encourage managers to have some autonomy to innovate, unlike that of a unit within the parent. Meanwhile, foreign-owned corporations may have a different corporate culture regarding risk taking.

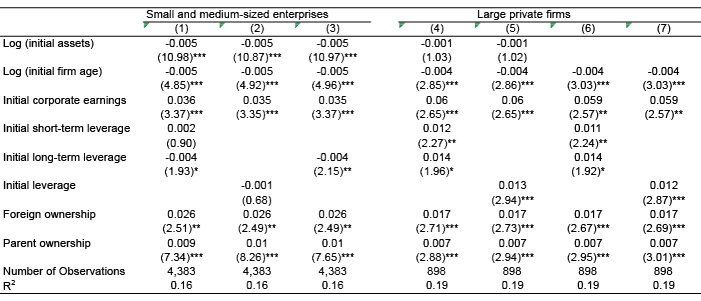

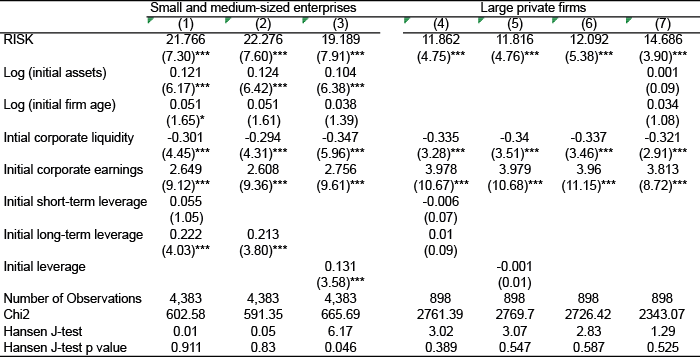

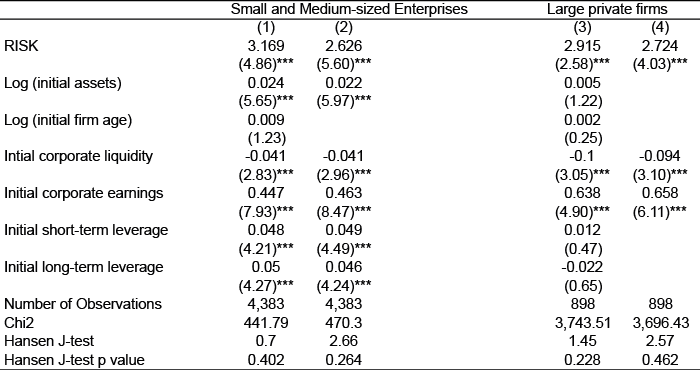

The ambiguities regarding risk taking of private firms motivate our empirical investigation (see Xu 2015 for details). We use the micro databases of the Basic Survey of Japanese Business Structure and Activities conducted by the Ministry of Economy, Trade and Industry and the Basic Survey on Small and Medium Enterprises conducted by the Small and Medium Enterprise Agency. The main purpose of the surveys is to acquire collective and quantitative information on diversification, globalisation, internationalisation, and the soft economy of Japanese enterprises. We provide empirical evidence of the relation between instrumented risk taking and both company assets and sales growth, as well as the relationship between ownership and risk taking.

Our main hypothesis is that foreign-owned affiliated private firms are more favourable to risk taking than domestically owned private firms. Also, we hypothesise that risk taking is positively related to firm growth and corporate earnings.

Risk taking and corporate earnings of private firms

According to our regression results, whole foreign ownership is associated with a 69.5% (40.8%) rise in risk taking above its mean. A one standard deviation increase in risk taking raises the annual "earnings before interest, tax, depreciation and amortisation"/assets ratio of small and medium-sized business by 4.8%, and of large private firms by 3.5%. It is notable that over the sample period 2003-2012, the same average annual ratio is only 6.9% for small and medium-sized firms and 9.1% for large private firms. Our results are consistent with John et al. (2008). Additionally, higher risk-taking firms had smaller cash flow shortfalls during the credit crisis of 2008-2009.

Foreign-owned private firms are much more inclined to risk-taking than domestically owned private firms. Risk taking has statistically and economically significant effects on corporate earnings. Moreover, poor performance during the crisis is relevant to our proxy for risk taking.

Our findings indicate that inward foreign direct investment has been changing corporate Japan by pursuing value-enhancing risk taking, in contrast with extremely high level of risk avoidance in Japan. This suggests that foreign-owned firms are more likely to take prompt action against poor or unsatisfactory corporate earnings than would corporate Japan. Such prompt action results in higher risk taking, and active risk taking is positively related to firm growth and corporate earnings. Japan promotes inward foreign direct investment by being "the best country in the world in which to do business" (Invest Japan, Cabinet Office). We conjecture that attracting inward foreign direct investment would not only increase the inflow of superior technologies and new expertise, but also import a new corporate culture of undertaking value-enhancing, yet risky actions promptly.

This article first appeared on www.VoxEU.org on August 3, 2015. Reproduced with permission.