| Author Name | SEKIZAWA Kumi (Ministry of Economy, Trade and Industry) |

|---|---|

| Research Project | Firm Dynamics, Industry, and Macroeconomy |

| Download / Links |

This Non Technical Summary does not constitute part of the above-captioned Discussion Paper but has been prepared for the purpose of providing a bold outline of the paper, based on findings from the analysis for the paper and focusing primarily on their implications for policy. For details of the analysis, read the captioned Discussion Paper. Views expressed in this Non Technical Summary are solely those of the individual author(s), and do not necessarily represent the views of the Research Institute of Economy, Trade and Industry (RIETI).

1. Background and Purpose

Japan is facing a declining population, making it essential to attract foreign direct investment (FDI) for economic growth. The government has set a target to achieve a balance of 100 trillion yen in inward FDI by 2030, but the current FDI-to-GDP ratio is significantly lower than the OECD average. This study aims to provide insights into factors that promote inward investment by analyzing FDI in OECD countries using the gravity model.

2. Research Approach

This study uses data on direct investment in OECD countries to clarify the conditions necessary for attracting FDI. It particularly focuses on the effective corporate tax rate and industrial structure, exploring their impact on FDI.

3. Main Analytical Method

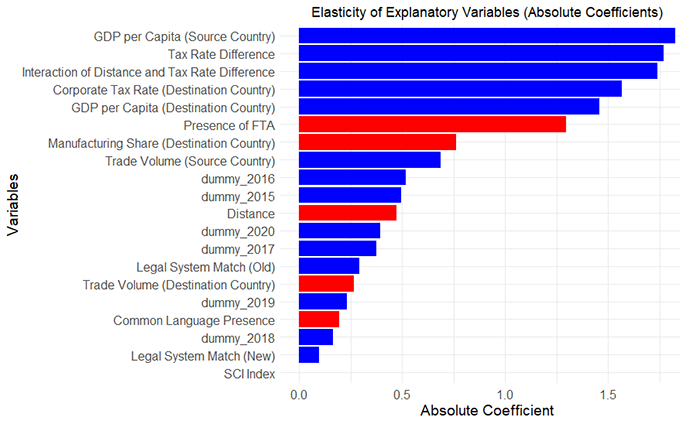

Using the gravity model, the study analyzes how factors such as bilateral economic size, distance, effective corporate tax rates, and the proportion of manufacturing industries affect FDI. The Poisson pseudo-maximum likelihood estimation method is used to appropriately include small countries with low levels of inward investment in the analysis.

4. Research Results

The analysis revealed the following findings:

- Impact of Effective Corporate Tax Rates: It has been shown that even when the effective corporate tax rate in the host country is high, FDI tends to be attracted. While this interpretation should be made with caution as other variables affecting FDI have been excluded, it could be noted that this may indicate that countries with high tax rates provide better social security and infrastructure, making them more appealing for investment.

- Tax Rate Differentials: FDI tends to increase when the effective corporate tax rate in the host country is lower than that in the investing country. Notably, the influence of this differential becomes stronger as the distance increases.

- Impact of Industrial Structure: It was suggested that Japan's high proportion of manufacturing industries negatively affects FDI. Countries with a strong manufacturing base face higher costs and competition, making them less attractive for foreign investment.

5. Policy Implications

The findings indicate that attention should be focused on the differential in tax rates between countries rather than the tax rate itself. Additionally, Japan's high manufacturing ratio may hinder its ability to attract FDI. This suggests that Japan, with its high corporate tax rate and significant manufacturing sector, may be at a disadvantage in attracting investment.

Simulation results showed that reducing Japan's corporate tax rate by 0.5% to 2% would decrease investment in the host country while increasing investment in Japan. This occurs because the narrowing of tax rate differentials reduces incentives for investment in the host country while enhancing Japan's relative attractiveness.

Moving forward, it is essential to consider the advantages and disadvantages of lowering Japan's corporate tax rate while also focusing on developing the ability to generate income in sectors beyond manufacturing.