With the passage of Trade Promotion Authority ("fast track") by the U.S. Congress, the pathway for completion of decade-long negotiations of the Trans-Pacific Partnership (TPP) has finally opened. The TPP is a projected agreement that would liberalize international trade and investment among twelve nations bordering the Pacific, including Japan and the U.S. Significantly, the TPP would not include China.

Abenomics is, of course, the suite of policies to revive the Japanese economy proposed by Prime Minister Shinzo Abe (http://www.japan.go.jp/_userdata/abenomics/150608_abenomics.pdf). In his well-received address to the U.S. Congress in April, the Prime Minister focused on the economic and strategic benefits of the TPP. The TPP is the keystone of his growth strategy for Japan and he has already identified many of the industries that will be the focus of reform initiatives to create new opportunities for trade and investment in Japan.

In a May 2015 report of the Research Institute of Economy, Trade and Industry (RIETI), a study led by Koji Nomura of Keio University (http://www.rieti.go.jp/jp/publications/dp/15e054.pdf) in collaboration with Jon Samuels of the U.S. Bureau of Economic Analysis and myself has analyzed price competitiveness between U.S. and Japanese industries over the period 1955-2012. Price competitiveness between the two countries is usually expressed in terms of the over- or under-valuation of the Japanese yen relative to the U.S. dollar. By comparing the relative price for all commodities purchased in the two countries with the market exchange rate of the yen and the dollar, we obtain our measure of price competitiveness.

We refer to the price of a commodity in Japan, expressed in yen, relative to the price in the U.S., expressed in terms of dollars, as the purchasing power parity. As a specific illustration, the purchasing power parity of a unit of the Gross Domestic Product (GDP) in Japan and the U.S. in 2005 was 124.9 yen per dollar, while the market exchange rate was 110.2 yen per dollar. The ratio between the two is the measure of price competitiveness, so that the yen was over-valued relative to the dollar by 13% in 2005. Firms located in Japan had to overcome a 13% price disadvantage in international markets to compete with U.S. producers.

A similar definition can be used at the level of individual commodities.

From the recovery of sovereignty by Japan in 1952 until the Plaza Accord of 1985, the yen was under-valued relative to the U.S. dollar. This provided an opportunity for Japan to grow rapidly by mobilizing its high quality labor force, maintaining high rates of capital formation, and dramatically improving productivity. Productivity is defined as output per unit of all inputs; this definition can be contrasted with labor productivity or output per hour worked.

Double-digit growth in Japan ended with the first oil shock of 1973, but the Japanese economy continued to grow more rapidly than the U.S. until the collapse of the "bubble economy" in Japan in 1991. Over-valuation of the yen relative to the dollar began with the Plaza Accord of 1985 and reached a peak in 1995. This precipitated a slump in Japanese exports and a slowdown in economic growth. The Japanese growth slowdown was marked by much lower capital formation, a decline in employment, and disappearance of productivity growth.

Since 1995, Japanese policy-makers have spent two decades dealing with the over-valuation of the yen, often called the Lost Decades. The exchange rate approached the yen-dollar purchasing power parity in 2007. However, the financial and economic crisis that originated in the U.S. in 2007-2009 led to a second sharp revaluation of the yen. Under Chairman Ben Bernanke, the Federal Reserve vastly expanded its balance sheet through quantitative easing, but the Bank of Japan under Governor Masaaki Shirakawa did not react.

In November 2011 the yen appreciated to historic highs relative to the dollar. Subsequently the yen depreciated modestly, but the yen was still substantially over-valued when Prime Minister Abe assumed office in December 2012. Depreciation of the yen accelerated with the adoption of quantitative easing by the Bank of Japan after Governor Haruhiko Kuroda was appointed in March 2013. Japanese price competitiveness vis-à-vis the United States was finally restored in February 2015.

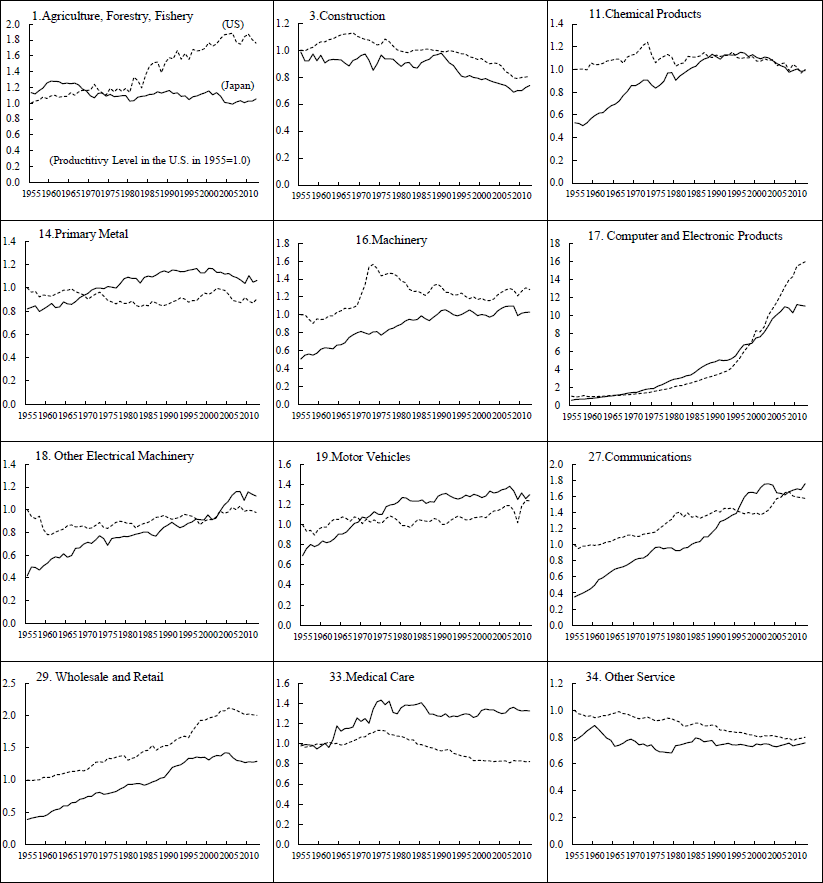

Price competiveness between Japan and the U.S. has a real counterpart in the productivity gaps between the two countries. Japan-U.S. productivity gaps for 1955-2012 from our study are shown in Figure 1. The white dots represent the overall productivity gaps, while productivity gaps for manufacturing are shown in black and for non-manufacturing in white.

In 1955, three years after Japan recovered sovereignty in 1952, Japanese productivity was more than 50% below that in the U.S. The gap closed gradually for more than three decades and Japan achieved near-parity with the U.S. in 1991. Over the following two decades productivity growth in Japan languished, while U.S. productivity growth slightly accelerated. As shown in Figure 1, the Japan-U.S. productivity gap reversed its long decline after 1991, rising by 2012 to levels of the early 1980s.

Our study for RIETI shows that productivity gaps for Japanese and U.S. manufacturing industries, especially those involved in materials processing rather than assembly, are relatively small. As indicated in Figure 2, the Japanese Motor Vehicles industry has had a higher level of productivity than its U.S. counterpart since the 1970s, but the productivity gap almost closed after the drastic re-organization of the U.S. industry in the aftermath of the financial and economic crisis of 2007-2009.

Two industries stand out in Figure 2 as opportunities for improvement in productivity. Medical Care in Japan has had a stable level of productivity since the mid-1970s, while the medical care industry in the United States has had consistently declining productivity. No doubt substantial improvements are possible in the measurement of medical care in Japan and U.S. However, the measured decline in U.S. productivity is unlikely to disappear. A revival of productivity growth would require major institutional reforms, but this would help to relieve budgetary pressure from spiraling health care costs at every level of the U.S. government.

[Click to enlarge]

Turning to opportunities for Japan, Japanese Agriculture has had no productivity growth since the mid-1970s, while its U.S. counterpart has achieved consistent and high rates of productivity growth. Agriculture has been targeted by the Abe Administration as a potential opportunity for rapid productivity growth. However, this would require major institutional changes, beginning with the Japanese system of agricultural co-operatives. These co-operatives have added enormously to the costs of agricultural production and distribution in Japan and have undermined growth in Japanese standards of living.

Additional opportunities for productivity improvements in Japan can be found in Figure 2. Six non-manufacturing industries that are largely insulated from international competition--Real Estate, Electricity and Gas, Construction, Other Services, Finance and Insurance, and Wholesale and Retail Trade--are also protected from domestic competition through government regulation of pricing and entry. Exploiting opportunities to improve productivity would require lowering barriers to entry, eliminating regulations that limit price competition, and encouraging both inward and outward foreign direct investment.

The two Lost Decades in Japan and the financial and economic crisis that began in the United States in 2007-2009 have created important untapped opportunities for economic growth in both countries. The TPP could help to revive economic growth in the United States by stimulating trade and investment. The greatest payoffs for Japan would come from combining the TPP with domestic reforms and encouraging Foreign Direct Investment. This would provide a growth strategy for Japan that could finally end the lost decades.

* Translated by RIETI.

July 21, 2015 Nihon Keizai Shimbun