On August 11, 2015, the People's Bank of China (PBOC) announced a policy of setting the midpoint rate of the yuan against the U.S. dollar, the benchmark for market transactions, at 6.2298, 1.8% weaker than the previous day, and using the previous day's closing market rate as a reference when setting the midpoint rate from then onwards. The purpose of the former is to correct the exchange rate of the yuan, which had become overvalued due to the depreciation of the euro and the yen, by devaluing it. The latter can be regarded as a major step in shifting from the current managed floating exchange rate system to a free floating exchange rate system for the yuan.

Background of the devaluation of the yuan and the future outlook

The magnitude of devaluation on August 11 is the largest since the current managed floating exchange rate system was introduced in July 2005. The midpoint rate of the yuan against the dollar subsequently continued to fall, reaching 6.3306 on August 12 and 6.4010 on August 13, or 4.7% in total for the three days.

Before that, the authorities had been fine-tuning the midpoint rate against the U.S. dollar in concert with the policy objective of maintaining macroeconomic stability (discussed below). However, with major currencies such as the euro and the yen depreciating sharply against the dollar, the yuan had surged against these currencies and, by extension, on an effective basis (weighted by trade with major trading partners) (Figure 1). The fact that foreign exchange reserves have shifted to a declining trend after peaking at $3.99 trillion in June 2014 (falling to $3.65 trillion in July 2015) also suggests that the yuan has become overvalued relative to the equilibrium level that reflects the supply-demand balance in the market and has faced downward pressure (Figure 2).

")

Exports from China (in dollar terms) declined 0.8% year on year in the first seven months this year, and the drop was particularly sharp in July 2015 when they fell by 8.3% year on year, partly reflecting the weak global economy. Stagnant exports have put a further damper on economic growth, which has been slowing down against the backdrop of the correction of the housing market. Major macroeconomic data in July point to a weak economy, and there is concern as to whether the annual growth target of 7% set by the government can be achieved (the actual growth rate for the first half was 7.0%). The purpose of the devaluation of the yuan on this occasion is no doubt to underpin the economy by boosting exports.

At present, the daily fluctuations of the yuan are limited to 2% above and below the midpoint rate against the dollar set by the authorities. However, if the market rate declines to the lower limit every day and the authorities adopt the closing rate of the previous day as the midpoint rate, it will be possible to devalue the yuan significantly over a short term even under the current system (e.g., if a fall of 2% continues for 10 days, the yuan will fall by more than 20% due to compounding). However, given that a significant fall in the yuan could intensify trade friction with developed countries such as the United States and provoke capital outflow from China and competitive devaluation involving developing countries including those in Southeast Asia, China needs to take a more cautious stance regarding further devaluation.

In fact, at the press conference held by the PBOC on August 13, 2015, Deputy Governor Yi Gang said, "It is completely groundless to say that the yuan will be devalued by about 10% to boost exports." Assistant Governor Zhang Xiaohui also pointed out, "The yuan is still a strong currency and will be gradually stabilized." "There is no basis for a continued depreciation of the yuan. It will return to the appreciation track in the future." These comments by the authorities are taken as a commitment by the authorities to end the latest round of devaluation of the yuan.

Progress with the reform of the yuan

Meanwhile, China is seeking to make its yuan exchange rate more flexible, and the adoption of the policy to use the closing rate in the market on the previous day as a reference when setting the midpoint rate can be regarded as part of this reform. In addition, the constituent currencies of the special drawing rights (SDR) of the International Monetary Fund (IMF) are planned to be reviewed by the end of the year, and the yuan is the only candidate under consideration. The latest move has been interpreted as a measure taken by the Chinese authorities to appeal to the IMF regarding the progress made in the yuan's transition to a floating exchange rate system (see Box).

In July 2005, in the name of "yuan reform," China shifted from a de facto dollar peg system to the current managed floating exchange rate system based on the so-called BBC rules consisting of a fluctuation band, a basket of currencies, and crawling (fine-tuning the exchange rate). Under this system, as the monetary authorities have to intervene in the market on a daily basis to ensure that the exchange rate stays within the predetermined fluctuation band, the aspect of "managed" is still stronger than that of "floating."

First, the authorities announce the midpoint rate of the yuan against the dollar every day before transactions begin, and the exchange rate is allowed to fluctuate within a certain range centering upon it. The fluctuation band was initially set at 0.3% above and below the midpoint rate, and it was widened to 0.5% on May 21, 2007, 1.0% on April 16, 2012, and 2.0% on March 17, 2014. It is unclear how the midpoint rate was determined, but since August 12, 2015, the midpoint rate has been set at a level close to the closing rate on the previous day, as defined in the new policy (Figure 3). However, as long as the closing rate on the previous day is strongly affected by the intervention of the authorities, there is no guarantee that the midpoint rate that is set by reference to the closing rate fully reflects the supply-demand balance in the market.

With respect to the basket of currencies, the authorities adjust the midpoint rate in consideration of the fluctuations of the currencies of other major trading partners against the dollar, while placing the focus of the exchange rate policy on the stability of the yuan against the dollar. The authorities attempt to stabilize the effective exchange rate of the yuan through such an adjustment. However, judging from the fact that the yuan's exchange rate against the dollar is much more stable than its effective exchange, the weight of the dollar in the currency basket used as a reference is extremely heavy.

As for the crawling pace, the midpoint rate rose by about 35% from July 2005, when China shifted to the managed floating exchange rate system, until August 10, 2015 immediately before the devaluation was implemented on this occasion.

Determinants of the midpoint rate of the yuan in the past

Even before the latest round of reform, the daily midpoint rate of the yuan and, by extension, the pace of crawling had never been constant, and had been adjusted in concert with the government's policy objective of maintaining macroeconomic stability. Reflecting this, the year-on-year rate of increase in the midpoint rate tends to be large (small) when the economic growth rate and the inflation rate are high (low).

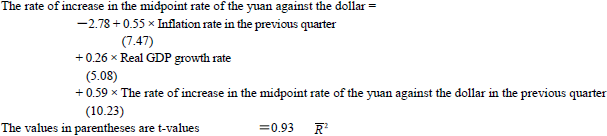

To confirm this relationship, which can be interpreted as a type of "reaction function of the exchange rate policy" in China, I conducted a regression analysis with the midpoint rate of the yuan against the dollar (year on year) as an explained variable and the inflation rate and the economic growth rate (both are year on year) as explanatory variables. In the analysis, I used the inflation rate from the previous quarter, rather than from the current quarter, taking into account the time lag between variables and the inertia of the exchange rate, and added the midpoint rate in the previous quarter to the explanatory variables. By doing so, I obtained the estimated result that the midpoint rate (year on year) tends to rise (fall) 0.55% against a 1% rise (fall) in the inflation rate in the previous quarter and rise (fall) 0.26% against a 1% rise (fall) in the economic growth rate (Figure 4). This reflects the fact that the authorities used the exchange rate as a means of stabilizing economic growth and prices.

The midpoint rate of the yuan against the dollar is the average of those in each period.

Estimation period: 3Q/2005 to 2Q/2015

As in the case of a fixed exchange rate, the exchange rate determined in concert with the authorities' policy does not necessarily come into line with an equilibrium rate that reflects the supply-demand balance in the market, and foreign exchange intervention is essential to maintain the exchange rate. The link between intervention and the monetary base makes it difficult for the authorities to control the money supply and reduces the effectiveness of monetary policy.

Specifically, if the midpoint rate of the yuan against the dollar is set at a level that is undervalued compared with the equilibrium rate that reflects the supply-demand balance in the market, the authorities must conduct dollar-buying intervention to keep the yuan from rising. In contrast, if the midpoint rate is set at a level that is more overvalued compared with the equilibrium rate, the authorities must conduct dollar-selling intervention to keep the yuan from falling (Figure 5). In the case of the former, foreign exchange reserves, the monetary base, and, by extension, the money supply (M2) will increase, and the accompanying expansion of liquidity will push up consumer prices and asset prices. In the case of the latter, foreign exchange reserves, the monetary base, and, by extension, the money supply will decrease, and the accompanying shrinkage of liquidity will lower consumer prices and asset prices.

From managed floating to free floating

The greatest aim of the yuan reform is to increase the independence of the monetary policy by allowing the exchange rate to fluctuate more freely. The independence of monetary policy varies significantly depending on the degree of freedom of capital mobility and the foreign exchange system. As the "impossible trinity" theory in international finance argues, no country is able to attain the three objectives of "free capital mobility," an "independent monetary policy," and a "fixed exchange rate" at the same time (Table 1). Until adopting a current managed floating system in 2005, China had long been trying to maintain an independent monetary policy by controlling capital mobility (abandoning free capital mobility) while maintaining a fixed exchange rate system, which was a de facto dollar peg system. However, as the yuan has become more widely used as an international currency and capital flow has become more and more active, the independence and, by extension, the effectiveness of monetary policy (interest-rate policy in particular) have declined.

Based on the impossible trinity theory, China currently adopts an "intermediate system" in which a certain level of fluctuations in exchange rates is permitted and capital mobility is also free to some extent. Under this system, a certain level of independence and effectiveness of monetary policy are maintained. To further enhance the independence and effectiveness of monetary policy, China must shift to a free floating exchange rate system.

Under the current managed floating exchange rate system, however, the authorities continue to play a decisive role in determining the yuan's exchange rate through intervention and the setting of the midpoint rate. To shift to a free floating exchange rate system, in which exchange rates are determined by market forces, the authorities eventually will have to terminate the announcement of the midpoint rate and refrain from foreign exchange intervention. Given that a specific schedule has yet to be announced, it may take some time before this transition process is finally completed.

Box: The Chinese yuan has become the leading candidate for the expansion of the constituent currencies of the SDR

The special drawing rights (SDR) are an international reserve asset established by the International Monetary Fund (IMF) in 1969 as a means of complementing the reserve assets of the member countries. The constituent currencies of the SDR have to be (1) four currencies issued by the member countries of the IMF and the currency union, which had the largest export of goods and services for the five years from 12 months before the effective date of the new composition ratio and (2) the currencies that were certified by the IMF as freely usable currencies pursuant to Article 30 (f) of the Articles of Agreement of the IMF. The current composition of the SDR that came into effect on January 1, 2011 is the U.S. dollar 41.9%, the euro 37.4%, the pound sterling 11.3%, and the Japanese yen 9.4%.

The composition of the SDR is reviewed every five years, and 2015 is the year of the revision. Attention is being focused on whether the Chinese yuan will become a constituent currency of the SDR and, if so, what weight it will have. The final decision is scheduled to be made by the end of the year. As the yuan has already met condition (1), the point of the review will be whether it has met condition (2).

Article 30 (f) of the Articles of Agreement of the IMF states, "A freely usable currency means a member's currency that the Fund determines (i) is, in fact, widely used to make payments for international transactions, and (ii) is widely traded in the principal exchange markets." In fact, the IMF emphasizes in the interim review of the SDR Basket conducted in 2015, "The concept of a freely usable currency concerns the actual international use and trading of currencies, and is different from whether a currency is either freely floating or fully convertible." (IMF, "IMF Work Progresses on 2015 SDR Basket," August 4, 2015). Thus, the assessment will be based on the progress in the "internationalization of the yuan," rather than the progress in the "yuan reform."

The IMF announced on August 19, 2015 that it would extend the period of validity of the current SDR Basket from the end of this year until September 2016. It explained that "the nine-month extension is intended to facilitate the continued smooth functioning of SDR-related operations and responds to feedback from SDR users on the desirability of avoiding changes in the basket at the end of the calendar year." The step taken this time should be regarded not as an implication that the adoption of the yuan as the SDR was shelved, as reported by some media, but as a measure to avoid confusion when a new basket including the yuan is adopted.

The original text in Japanese was posted on September 10, 2015.